Brisbane Unit – 1 bed 1 bath

South Brisbane QLD 4101

Tax Depreciation

T.D559,663 over 40 years

$645,000

Learn More

Thornlands Shopping Centre QLD

Thornlands QLD 4164

Shops & Retail

T.D$424,197 over 40 years

$1,925,000

Learn More

Kings Meadows TAS-4 Beds 2 Bath

Kings Meadows TAS 7249

Tax Depreciation

T.D$599,576 over 40 years

$579,767

Learn More

Maroochydore QLD- 4 Beds 3 Bath

Maroochydore QLD 4558

Tax Depreciation

T.D$283,436 over 37 years

$685,000

Learn More

Baldivis WA- 3 Beds 2 Bath

Baldivis WA 6171

Tax Depreciation

T.D$99,318 over 30 years

$358,200

Learn More

Brassall Bakery Shop QLD

Brassall QLD 4305

Shops & Retail

T.D$125,900 over 40 years

$120,000

Learn More

Burleigh Heads Factory Warehouse QLD

Burleigh Heads QLD 4220

Factory, Warehouse & Industrial

T.D$361,228 over 40 years

$745,000

Learn More

Yatala Factory Warehouse QLD

Yatala QLD 4207

Warehouse, Factory & Industrial • Offices

T.D$1,448,276 over 40 years

$1,475,000

Learn More

St Lucia QLD- 2 Beds 2 Bath

St Lucia QLD 4067

Tax Depreciation

T.D$60,226 over 40 years

$455,000

Learn More

Macleod VIC- 3 Beds 2 Bath

Macleod VIC 3085

Tax Depreciation

T.D$158,543 over 40 years

$868,000

Learn More

Hope Island QLD- 5 Beds 4 Bath

Hope Island QLD 4212

Tax Depreciation

T.D$448,515 over 39 years

$2,165,000

Learn More

Malvern East VIC- 4 Beds 2 Bath

Malvern East VIC 3145

Tax Depreciation

T.D$65,690 over 40 years

$1,900,000

Learn More

Wattle Grove WA- 3 Beds 2 Bath

Wattle Grove WA 6107

Tax Depreciation

T.D$640,000

$173,196 over 30 years

Learn More

Maroochydore QLD- 2 Beds 2 Bath

Maroochydore QLD 4558

Tax Depreciation

T.D$373,872 over 40 years

$675,000

Learn More

Eight Mile Plains QLD- 4 Beds 1 Bath

Eight Mile Plains QLD 4113

Tax Depreciation

T.D$581,235 over 40 years

$630,000

Learn More

Ellenbrook WA- 3 Beds 2 Bath

Ellenbrook WA 6069

Tax Depreciation

T.D$141,134 over 35 years

$439,221

Learn More

Melton South VIC- 4 Beds 2

Melton South VIC 3338

Tax Depreciation

T.D$216,106 over 40 years

$219,097

Learn More

Brinsmead QLD- 4 Beds 2 Bath

Brinsmead QLD 4870

Tax Depreciation

T.D$85,414 over 40 years

$555,000

Learn More

Greenway ACT- 2 Beds 2 Bath

Greenway ACT 2900

Tax Depreciation

T.D$378,371 over 40 years

$474,000

Learn More

Redland Bay QLD- 3 Beds 2 Bath

Redland Bay Qld 4165

Tax Depreciation

T.D$172,992 over 40 years

$173,500

Learn More

Caringbah Small Storage NSW

Caringbah NSW 2229

Factory, Warehouse & Industrial

T.D$46,817 over 40 years

$175,000

Learn More

Southport Facefit Skincare Clinic QLD

Southport QLD 4215

Personal Care Services

T.D$253,277 over 40 years

$253,277

Learn More

Salisbury Factory Warehouse QLD

Salisbury QLD 4107

Factory, Warehouse & Industrial

T.D$512,885 over 40 years

$1,062,000

Learn More

Mount Barker SA- 4 Beds 2 Bath

Mount Barker SA 5251

Tax Depreciation

T.D$270,910 over 40 years

$495,000

Learn More

Surfers Paradise Boulevard QLD- 2 Beds 1 Bath

Surfers Paradise QLD 4217

Tax Depreciation

T.D$41,054 over 39 years

$335,000

Learn More

Kingston ACT- 2 Beds 1 Bath

Kingston ACT 2604

Tax Depreciation

T.D$236,080 over 40 years

$480,000

Learn More

Collingwood VIC- 1 Bed 1 Bath

Collingwood Vic 3066

Tax Depreciation

T.D$54,388 over

$520,000 over 26 years

Learn More

Port Macquarie NSW- 2 Beds 2 Bath

Port Macquarie NSW 2444

Tax Depreciation

T.D$348,515 over 40 years

$1,000,000

Learn More

West End QLD- 2 Beds 2 Bath

West End Qld 4101

Tax Depreciation

T.D$324,853 over 40 years

$496,335

Learn More

Broadbeach QLD- 2 Beds 2 Bath

Broadbeach QLD 4218

Tax Depreciation

T.D$189,498 over 40 years

$890,000

Learn More

Sunnybank Hills QLD- 3 Beds 2 Bath

Sunnybank Hills Qld 4109

Tax Depreciation

T.D$186,131 over 4 years

$1,175,000

Learn More

Paddington QLD- 3 Beds 1 Bath

Paddington QLD 4064

Tax Depreciation

T.D$32,017 over 24 years

$1,119,500

Learn More

Surfers Paradise QLD- 3 Beds 2 Bath

Surfers Paradise QLD 4217

Tax Depreciation

T.D$676,213 over 40 years

$1,050,000

Learn More

Glenside SA- 2 Beds 1 Bath

Glenside SA 5065

Tax Depreciation

T.D$43,207 over 40 years

$740,000

Learn More

Oaklands Park SA- 3 Beds 1 Bath

Oaklands Park SA 5046

Tax Depreciation

T.D$123,636 over 31 years

$405,000

Learn More

St Johns Park NSW- 6 Beds 2 Bath

St Johns Park NSW 2176

Tax Depreciation

T.D$176,268 over 36 years

$1,228,000

Learn More

Liverpool NSW- 2 Beds 2 Bath

Liverpool NSW 2170

Tax Depreciation

T.D$363,471 over 40 years

$564,000

Learn More

Rockhampton City QLD (Rooming House) 21 Beds 8 Baths

Rockhampton City QLD 4700

Tax Depreciation

T.D$557,902 over 40 years

$430,000

Learn More

Burleigh Heads Factory Warehouse QLD

Burleigh Heads QLD 4220

Factory, Warehouse & Industrial

T.D$82,399 over 29 years

$1,040,000

Learn More

Greenway ACT- 2 Beds 1 Bath

Greenway ACT 2900

Tax Depreciation

T.D$347,084 over 40 years

$429,000

Learn More

Helensvale QLD- 4 Beds 3 Bath

Helensvale QLD 4212

Tax Depreciation

T.D$608,691 over 37 years

$1,800,000

Learn More

Office Fit out Brisbane City QLD

Brisbane City QLD 4000

Office Fitout

T.D$1,500,774 over 40 years

$1,500,774

Learn More

Cincotta Discount Chemist Indooroopilly QLD

Indooroopilly QLD 4068

Pharmacy

T.D$1.220,014 over 40 years

$4,470,000

Learn More

Lennox Head Pharmacy NSW

Lennox Head NSW 2478

Pharmacy

T.D$645,124 over 40 years

$3,600,000

Learn More

Banksmeadow Office Fitout NSW

Banksmeadow NSW 2019

Office

T.D$100,085 over 40 years

$970,000

Learn More

North Manly NSW- 4 Bed 3 Bath

North Manly NSW 2100

Tax Depreciation

T.D$233,982 over 40 years

$1,740,000

Learn More

Box Hill VIC- 2 Beds 2 Bath

Box Hill VIC 3128

Tax Depreciation

T.D$606,903 over 40 years

$959,500

Learn More

Currumbin QLD- 2 Beds 2 Bath

Currumbin QLD 4223

Tax Depreciation

T.D$1,275,000

$65,597 over 40 years

Learn More

Brookdale WA- 4 Beds 2 Bath

Brookdale WA 6112

Tax Depreciation

T.D$33,287 over 40 years

$310,000

Learn More

Dayton WA- 3 Beds 2 Bath

Dayton WA 6055

Tax Depreciation

T.D$37,513 over 40 year

$433,000

Learn More

Baulkham Hills NSW- 4 Beds 2 Bath

Baulkham Hills NSW 2153

Tax Depreciation

T.D$46,602 over 40 years

$1,935,000

Learn More

Oasis Centre Slacks Creek QLD

Slacks Creek QLD

Shops & Retail

T.D$4,345,232 over 40 years

$9,300,000

Learn More

Noosaville Factory Warehouse QLD

Noosaville QLD

Factory Warehouse

T.D$217,698 over 40 years

$750,000

Learn More

Harrisdale WA- 4 Beds 2 Bath

Harrisdale WA

Tax Depreciation

T.D$55,676 over 40 years

$610,000

Learn More

Office Fitout Underwood QLD

Underwood QLD 4119

Office Fitout

T.D$907,113 over 40 years

$1,461,888

Learn More

Goonellabah NSW 2480

Goonellabah NSW 2480

Warehouse, Factory & Industrial • Offices

T.D$502,712

$935,000

Learn More

Greenslopes QLD – 2 bed 2 bath

Greenslopes QLD

Tax Depreciation

T.D$47,136 over 40 years

$518,000

Learn More

Industrial Warehouse Dandenong South VIC

Dandenong South VIC

Warehouse, Factory & Industrial

T.D$4,341,128 over 40 years

$28,090,909

Learn More

Industrial Warehouse Smithfield NSW

Smithfield NSW

Warehouse, Factory & Industrial

T.D$9,517,401 over 40 years

$9,517,401

Learn More

Kingsgrove Factory Warehouse NSW

Kingsgrove, NSW 2208

Factory, Warehouse & Industrial

T.D$3,901,786 over 40 Year

$37,000,000

Learn More

Prime Spec Warehouse QLD

Pinkenba QLD 4008

Warehouse, Factory & Industrial

T.D$6,190,440

$6,305,591

Learn More

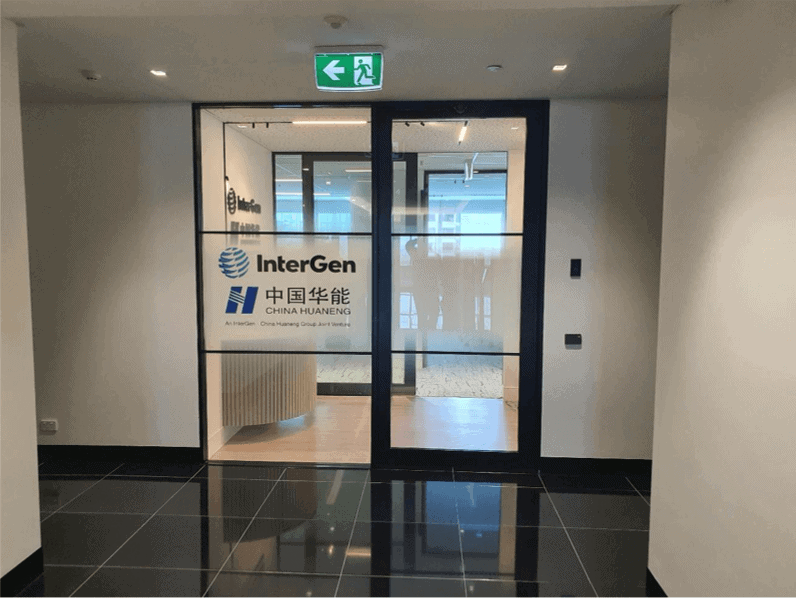

Intergen Office Fitout QLD

Brisbane City QLD 4000

Office Fitout

T.D$1,517,177 over 40 Years

$1,517,177

Learn More

Contentrix Office Fitout QLD

Brisbane City QLD 4000

Office Fitout

T.D$8,757,084 over 40 Years

$8,757,084

Learn More

Stanwell Energy Office Fitout QLD

Brisbane City QLD 4000

Office Fitout

T.D$662,360 over 40 Years

$662,360

Learn More

Jemena Fitout VIC

Broadmeadows VIC 3047

Office Fitout

T.D$13,490,823 over 40 Years

$13,535,418

Learn More

Foster & Partners Unit NSW

Sydney NSW 2000

Office Fit Out

T.D$245,490 Over 40 Years

$245,490

Learn More

Office Fit Out Macquarie Park NSW

MACQUARIE PARK, NSW 2113

Office Fit Out

T.D$8,820,138 for 40 Years

$8,820,138

Learn More

Uniting Care FitOut QLD

Brisbane City QLD 4000

Uniting Care Office Fit Out

T.D$9,882,158

$9,882,158

Learn More

North Rockhampton Nursing Home NSW

Norman Gardens QLD 4701

Life Cycle Report

The Riley Hotel QLD

Cairns City QLD 4870

Hotel

T.D$136,947,826 Over 40 years

$141,012,434

Learn More

Carlton VIC – 3 Beds 2 Bath

Carlton VIC 3053

Tax Depreciation

T.D$269,075 over 40 years

$429,000

Learn More

Altona Meadows VIC – 1 Beds 1 Bath

Altona Meadows VIC 3028

Tax Depreciation

T.D$142,999 over 37 years

$530,000

Learn More

Oxley QLD – 3 Beds 2 Bath

Oxley QLD 4075

Tax Depreciation

T.D$295,966 over 40 years

$499,900

Learn More

Kellyville NSW – 5 Beds 3 Bath

Kellyville NSW 2155

Tax Depreciation

T.D$506,297 over 40 years

$462,837

Learn More

Upper Mount Gravatt QLD – 2 Beds 2 Bath

Upper Mount Gravatt QLD 4122

Tax Depreciation

T.D$200,334 over 35 years

$405,000

Learn More

Pomona QLD – 6 Beds 4 Bath

Pomona QLD 4568

Tax Depreciation

T.D$579,266 over 40 years

$1,665,000

Learn More

Shopping Centre Acacia Ridge QLD

Acacia Ridge QLD 4110

Shops & Retail

T.D$153,676 Over 40 years

$146,325

Learn More

Belmont QLD – 3 Beds 2 Bath

Belmont QLD 4153

Tax Depreciation

T.D$79,260 over 40 years

$545,000

Learn More

Coomera QLD – 4 Beds 2 Bath

Coomera QLD 4209

Tax Depreciation

T.D$214,398 over 40 years

$498,000

Learn More

Newtown QLD – 4 Beds 2 Bath

Newtown QLD 4350

Tax Depreciation

T.D$3,347 over 37 years

$250,000

Learn More

Kingscliff NSW – 2 Beds 2 Bath

Kingscliff NSW 2487

Tax Depreciation

T.D$264,426 over 40 years

$810,000

Learn More

Eastgardens NSW – 2 Beds 2 Bath

Eastgardens NSW 2036

Tax Depreciation

T.D$328,767 over 40 years

$850,000

Learn More

Broadbeach Waters QLD – 4 Beds 3 Bath

Broadbeach Waters QLD 4218

Tax Depreciation

T.D$313,255 over 39 years

$1,730,000

Learn More

Highgate SA – 5 Beds 2 Bath

Highgate SA 5063

Tax Depreciation

T.D$151,241 over 40 years

$1,280,000

Learn More

Strathfield NSW – 2 Beds 2 Bath

Strathfield NSW 2135

Tax Depreciation

T.D$71,467 over 35 years

$810,000

Learn More

Broadbeach Waters QLD – 4 Beds 4 Bath

Broadbeach Waters QLD 4218

Tax Depreciation

T.D$302,476 over 39 years

$1,485,000

Learn More

Carrara Office Warehouse QLD

Carrara QLD 4211

Warehouse, Factory & Industrial • Offices

T.D$368,011 Over 40 years

$757,100

Learn More

Altona Meadows Medical Center VIC

Altona Meadows VIC 3028

Medical & Consulting

T.D$281,202 Over 40 years

$987,525

Learn More

Epping Warehouse VIC

Epping VIC 3076

Warehouse, Factory & Industrial • Showrooms & Large Format Retail • Offices

T.D$313,022 Over 40 years

$605,000

Learn More

Truganina Warehouse VIC

Truganina VIC 3029

Factory, Warehouse & Industrial

T.D$238,408 Over 40 years

$363,586

Learn More

Childcare Center QLD

Manoora QLD 4870

Medical & Consulting

T.D$616,567 Over 40 years

$2,387,383

Learn More

Rasoi Indian Gourmet Store NSW

Orange NSW 2800

Shops & Retail

T.D$85,858 Over 34 years

$640,000

Learn More

West Croydon SA – 2 Beds 1 Bath

West Croydon SA 5008

Tax Depreciation

T.D$28,328 over 39 years

$300,000

Learn More

Semaphore South SA – 2 Beds 1 Bath

Semaphore South SA 5019

Tax Depreciation

T.D$27,449 over 40 years

$380,000

Learn More

Tonsley SA – 2 Beds 2 Bath

Tonsley SA 5042

Tax Depreciation

T.D$174,964 over 40 years

$369,000

Learn More

Sellicks Beach SA – 3 Beds 2 Bath

Sellicks Beach SA 5174

Tax Depreciation

T.D$200,830 over 36 years

$365,000

Learn More

Mowbray TAS – 2 Beds 1 Bath

Mowbray TAS 7248

Tax Depreciation

T.D$99,377 over 33 years

$325,000

Learn More

Rokeby TAS – 3 Beds 2 Bath

Rokeby TAS 7019

Tax Depreciation

T.D$201,940 over 39 years

$425,000

Learn More

Belmont WA – 2 Beds 2 Bath

Belmont WA 6104

Tax Depreciation

T.D$144,478 over 40 years

$340,000

Learn More

Maddington WA – 4 Beds 3 Bath

Maddington WA 6109

Tax Depreciation

T.D$77,545 over 40 years

$520,000

Learn More

Narre Warren South VIC – 4 Beds 2 Bath

Narre Warren South VIC 3805

Tax Depreciation

T.D$345,771 over 40 years

$350,000

Learn More

Cranbourne VIC – 3 Beds 1 Bath

Cranbourne VIC 3977

Tax Depreciation

T.D$37,634 over 40 years

$334,000

Learn More

Southport Office Warehouse QLD

Southport QLD 4215

Warehouse, Factory & Industrial • Offices

T.D$692,843 Over 40 years

$1,950,000

Learn More

West End Retail Shop QLD

West End QLD 4101

Shops & Retail

T.D$334,597 Over 40 years

$271,022

Learn More

Wellcamp Warehouse QLD

Wellcamp QLD 4350

Factory, Warehouse & Industrial

T.D$8,029,501 Over 40 years

$5,618,409

Learn More

Helensvale Pharmacy QLD

Helensvale QLD 4212

Pharmacy

T.D$9808,819 Over 40 years

$2,150,000

Learn More

Southport Park Pharmacy QLD

Southport QLD 4215

Pharmacy

T.D$977,954 Over 40 years

$4,100,000

Learn More

Klemzig Medical Center SA

Klemzig SA 5087

Medical & Consulting

T.D$9,440,110 Over 40 years

$8,886,499

Learn More

Fortitude Cres Warehouse QLD

Burleigh Heads QLD 4220

Warehouse, Factory & Industrial

T.D$299,257 Over 40 years

$2,500,001

Learn More

TerryWhite Chemmart Bundaberg Pharmacy QLD

Bundaberg Central QLD 4670

Pharmacy

T.D$198,282 Over 40 years

$1,065,000

Learn More

Dam Lawyers QLD

Forest Lake QLD 4078

Tax Depreciation

T.D$739,253 Over 37 years

$187,595 (Fir-Out)

Learn More

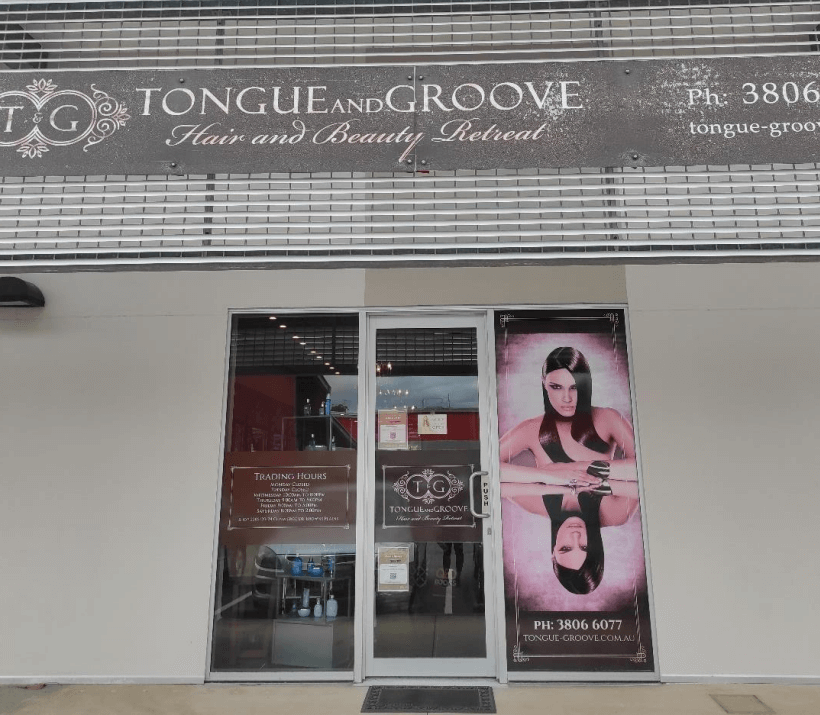

Tongue and Groove Hair and Beauty Retreat QLD

Brown Plains QLD 4118

Personal Care Services

T.D$96,720 Over 40 years

$500,000

Learn More

M Carvery – Beenleigh Marketplace QLD

Beenleigh QLD 4207

Tax Depreciation

T.D$274,903 Over 40 years

$48,065 (Fit-Out)

Learn More

The Saracen’s Head Hotel SA

Adelaide SA 5000

Tax Depreciation

T.D$2,182,498 Over 40 years

$3,575,000

Learn More

Duxton The Brompton Hotel SA

Brompton SA 5007

Tax Depreciation

T.D$2,155,758 Over 40 years

$3,000,000

Learn More

Priceline Pharmacy Traralgon VIC

Traralgon VIC 3844

Tax Depreciation

T.D$766,041 Over 36 years

$2,662,000

Learn More

Bloom Restaurant SA

Thebarton SA 5031

Tax Depreciation

T.D$700,000 Over 40 years

$700,000

Learn More

Tarneit VIC – 4 Beds 2 Bath

Tarneit VIC 3029

Tax Depreciation

T.D$256,866 over 40 years

$261,095

Learn More

North Melbourne VIC – 3 Beds 3 Bath

North Melbourne VIC 3051

Tax Depreciation

T.D$968,000

$154,614 over 30 years

Learn More

Dromana VIC – 3 Beds 1 Bath

Dromana VIC 3936

Tax Depreciation

T.D$96,069 over 40 years

$765,000

Learn More

Clyde VIC – 3 Beds 2 Bath

Clyde VIC 3978

Tax Depreciation

T.D$226,613 over 39 years

$533,000

Learn More

Burwood East VIC – 2 Beds 1 Bath

Burwood East VIC 3151

Tax Depreciation

T.D$248,958 over 40 years

$450,000

Learn More

High Spirits Wholesale Warehouse QLD

Tingalpa QLD 4173

Tax Depreciation

T.D$347,065 Over 40 years

$3,900,000

Learn More

Shopping Plaza QLD

Bray Park QLD 4500

Tax Depreciation

T.D$800,060 Over 40 years

$4,125,000

Learn More

Seafood Restaurant QLD

Cairns North QLD 4870

Tax Depreciation

T.D$73,559 Over 40 years

$295,000

Learn More

Batemans Bay NSW – 3 Beds 2 Bath

Batemans Bay NSW 2536

Tax Depreciation

T.D$217,048 over 32 years

$620,000

Learn More

Schofields NSW – 5 Beds 3 Bath

Schofields NSW 2762

Tax Depreciation

T.D$385,550 over 40 years

$548,000

Learn More

Mortdale NSW – 5 Beds 3 Bath

Mortdale NSW 2223

Tax Depreciation

T.D$1,680,000

$586,063 over 40 years

Learn More

Castle Hill NSW – 3 Beds 2 Bath

Castle Hill NSW 2154

Tax Depreciation

T.D$199,967 over 25 years

$930,000

Learn More

Gosford NSW – 2 Beds 2 Bath

Gosford NSW 2250

Tax Depreciation

T.D$326,630 over 40 years

$415,000

Learn More

Warehouse Factory & Industrial WA

Bibra Lake WA 6163

Tax Depreciation

T.D$38,7410 Over 35 years

$828,000

Learn More

Royal Oak Hotel SA

Penola SA 5277

Tax Depreciation

T.D$1,439,985 Over 40 years

$1,750,000

Learn More

Bushman’s Arms Hotel SA

Naracoorte SA 5271

Tax Depreciation

T.D$2,011,003 Over 40 years

$3,650,000

Learn More

Woolshed Inn Hotel SA

Bordertown SA 5268

Tax Depreciation

T.D$1,939,986 Over 40 years

$2,250,000

Learn More

Harrington Park NSW – 4 Beds 2 Bath

Harrington Park NSW 2567

Tax Depreciation

T.D$1,395,735 over 40 years

$1,800,000

Learn More

Carindale QLD – 5 Beds 3 Bath

Carindale QLD 4152

Tax Depreciation

T.D$110,448 over 32 years

$1,620,000

Learn More

Kewarra Beach QLD – 4 Beds 2 Bath

Kewarra Beach QLD 4879

Tax Depreciation

T.D$185,492 over 40 years

$495,000

Learn More

Toowong QLD – 3 Beds 3 Baths

Toowong, QLD 4066

Tax Depreciation

T.D$750,208 over 40 years

$139,000

Learn More

Old Noarlunga Hotel SA

Old Noarlunga SA 5168

Tax Depreciation

T.D$2,562,348 over 40 years

$11,000,000

Learn More

Commercial Offices QLD

South Brisbane QLD 4101

Tax Depreciation

T.D$594,459 over 40 years

$5,050,000

Learn More

Birkdale QLD – 4 Beds 2 Bath

Birkdale QLD 4159

Tax Depreciation

T.D$313,907 over 39 years

$710,691

Learn More

South Brisbane QLD – 2 Beds 2 Bath

South Brisbane QLD 4101

Tax Depreciation

T.D$372,773 over 40 years

$729,000

Learn More

Annerley QLD – 3 Beds 2 Bath

Annerley QLD 4103

Tax Depreciation

T.D$430,412 over 40 years

$449,296

Learn More

Gisborne VIC – 4 Beds 2 Bath

Gisborne VIC 3437

Tax Depreciation

T.D$330,066 over 40 years

$800,000

Learn More

Nedlands WA – 4 Beds 1 Bath

Nedlands WA 6009

Tax Depreciation

T.D$104,129 over 40 years

$1,840,000

Learn More

Commercial/Industrial Complex QLD

Upper Coomera QLD 4209

Tax Depreciation

T.D$238,251 Over 40 years

$518,000

Learn More

Commercial Centre QLD

Burleigh Waters QLD 4220

Tax Depreciation

T.D$140,579 Over 40 years

$450,000

Learn More

North Lakes Car Wash QLD

North Lakes QLD 4509

Tax Depreciation

T.D$473,503 over 40 years

$$447,994

Learn More

Lodges & Cottages QLD

Tamborine Mountain QLD 4272

Tax Depreciation

T.D$620,935 over 34 years

$2,500,000

Learn More

Sellicks Beach SA – 3 Beds 1 Bath

Sellicks Beach SA 5174

Tax Depreciation

T.D$22,266 over 40 years

$356,800

Learn More

Wakerley QLD – 4 Beds 2 Baths

Wakerley QLD 4154

Tax Depreciation

T.D$252,398 over 38 years

$711,021

Learn More

Acacia Ridge QLD – 3 Beds 1 Bath

Acacia Ridge QLD 4110

Tax Depreciation

T.D$23,920 over 40 years

$352,500

Learn More

Glen Waverley VIC – 2 Beds 1 Bath

Glen Waverley VIC 3150

Tax Depreciation

T.D$307,670 over 40 years

$560,888

Learn More

Langford WA – 2 Beds 1 Bath

Langford WA 6147

Tax Depreciation

T.D$50,510 over 40 years

$255,000

Learn More

Warehouse Factory & Industrial QLD

Molendinar QLD 4214

Tax Depreciation

T.D$1,892,000

$235,080 over 34 years

Learn More

Indoor Playground SA

Sefton Park SA 5083

Tax Depreciation

T.D$1,298,320 over 40 years

$2,033,624

Learn More

Industrial Building WA

Forrestdale WA 6112

Tax Depreciation

T.D$1,298,320 over 40 years

$1,300,000

Learn More

Retail Warehouse QLD

Bundall QLD 4217

Tax Depreciation

T.D$229,418 over 40 years

$3,190,000

Learn More

Shopping Centre QLD

Bundall QLD 4217

Tax Depreciation

T.D$684,080 over 40 years

$2,400,000

Carlton VIC – 2 Baths 2 Beds

Carlton VIC 3053

Tax Depreciation

T.D$295,092 over 40 years

$607,500

Learn More

Rouse Hill NSW – 2 Beds 2 Baths

Rouse Hill NSW 2155

Tax Depreciation

T.D$330,794 over 40 years

$645,000

Learn More

Rosehill NSW – 2 Beds 2 Baths

Rosehill NSW 2142

Tax Depreciation

T.D$269,160 over 40 years

$634,000

Learn More

Footscray VIC – 2 Beds 2 Baths

Footscray VIC 3011

Tax Depreciation

T.D$328,174 over 40 years

$535,500

Learn More

North Kellyville NSW – 2 Beds 2 Baths

North Kellyville NSW 2155

Tax Depreciation

T.D$331,607 over 40 years

$649,000

Learn More

Office Warehouse QLD

Mansfield QLD 4122

Tax Depreciation

T.D$89,832 over 31 years

$275,000

Learn More

Tool City QLD

Coopers Plains QLD 4108

Tax Depreciation

T.D$143,963 over 40 years

$639,000

Learn More

Medical Centre VIC

Longwarry VIC 3816

Tax Depreciation

T.D$379,999 over 40 years

$380,000 Construction cost

Learn More

Albion Rooftop Club VIC

South Melbourne VIC 3205

Tax Depreciation

T.D$3,412,497 over 40 years

$5,421,533

Learn More

Padstow NSW – 3 Beds 2 Baths

Padstow NSW 2211

Tax Depreciation

T.D$62,368 over 40 years

$480,000

Learn More

Hope Island QLD – 3 Beds 2 Baths

Hope Island QLD 4212

Tax Depreciation

T.D$59,413 over 21 years

$370,000

Learn More

Pimpama QLD – 3 Beds 2 Baths

Pimpama QLD 4209

Tax Depreciation

T.D$175,235 over 39 years

$491,000

Learn More

West End QLD – 3 Beds 2 Baths

West End QLD 4101

Tax Depreciation

T.D$175,235 over 39 years

$491,000

Learn More

Alderley QLD – 4 Beds 2 Bath

Alderley QLD 4051

Tax Depreciation

T.D$86,076 for 33 years

$1,005,000

Learn More

Lago Vista – 3 Beds 2 Baths

Lago Vista, Dubai

Tax Depreciation

T.D$164,214 over 40 years

$209,138

Learn More

Lakeside – 1 Beds 2 Baths

Lakeside, Dubai

Tax Depreciation

T.D$168,165 over 40 years

$226,506

Learn More

Corby NN18 8PZ – 3 Beds 2 Baths house

Corby NN18 8PZ UK

Tax Depreciation

T.D$232,305 over 40 years

$435,500

Learn More

Old Town Dubai – 1 Bed 2 Baths house

Old Town Dubai UAE

Tax Depreciation

T.D$329,641 over 40 years

$591,666

Learn More

West Moonah TAS – 6 Beds 4 Baths house

West Moonah TAS 7009

Tax Depreciation

T.D$750,000 over 40 years

$750,000

Learn More

Akaroa TAS – 3 Beds 2 Baths house

Akaroa TAS 7216

Tax Depreciation

T.D$239,414 over 40 years

$264,277

Invermay TAS – 2 Beds 1 Baths house

Invermay TAS 7248

Tax Depreciation

T.D$85,733 over 28 years

$287,500

Learn More

Port Sorell TAS – 3 Beds 3 Baths house

Port Sorell TAS 7307

Tax Depreciation

T.D$462,801 over 40 years

$1,150,000

Learn More

Myrtle Bank SA – 4 Beds 3 Baths

Myrtle Bank SA 5064

Tax Depreciation Report

T.D$435,985 over 40 years

$886,000

Learn More

Waterford QLD – 5 Beds 2 Baths

Waterford QLD 4133

Tax Depreciation Report

T.D$200,400 over 40 years

$430,000

Learn More

Macgregor QLD – 5 Beds 2 Baths

Macgregor QLD 4109

Tax Depreciation Report

T.D$179,138 over 40 years

$778,000

Learn More

Smithfield NSW – 3 Beds 1 Bath

Smithfield NSW 2164

Tax Depreciation Report

T.D$59,476 over 40 years

$458,000

Learn More

Retail Shop Kilda VIC

Kilda VIC 3182

Tax Depreciation Schedule

T.D$248,563 over 25 years

$1,130,000

Learn More

Precinct Hotel Cremorne VIC

Cremorne VIC 3121

Tax Depreciation Report

T.D$2,011,782 over 40 years

$2,011,787

Learn More

Office Fitout Pyrmont NSW

Pyrmont NSW 2009

Tax Depreciation Report

T.D$163,344 over 33 years

$397,500

Learn More

Warehouse Henderson WA

Henderson WA 6166

Tax Depreciation Schedule

T.D$1,074,270 over 40 years

$1,850,000

Learn More

Brisbane Valley Tavern and 3 stores Fernvale QLD

Fernvale QLD 4306

Tax Depreciation Report

T.D$1,095,527

$2,275,000

Learn More

Veterinary Clinic Miranda NSW

Miranda NSW 2228

Tax Depreciation Report

T.D$2,342,364 over 40 years

$2,150,000

Learn More

Craigieburn VIC – 4 Beds 2 Baths

Craigieburn VIC 3064

Tax Depreciation Report

T.D$240,811 over 40 years

Construction cost: $272,500

Learn More

Frankston South Vic – 4 Beds 3 Baths

Frankston South, VIC 3199

Tax Depreciation

T.D$451,684 over 40 years

Construction cost: ~$303,505

Learn More

House 4 Bed 3 bath (California, USA)

Manhattan Beach, CA 90266, USA

Tax Depreciation report

T.D$1,183,465 over 40 years

Purchase Price: ~$6,900,000

Learn More

Gumeracha SA – 4 Beds 1 Baths house

Gumeracha SA 5233

Tax Depreciation Report

T.D$84,774 over 40 years

Purchase Price: ~ $360,000

Learn More

Nollamara WA – 3 bed 2 bath house

Nollamara WA 6061

Tax depreciation report

T.D$234,761 over 39 years

Purchase Price: $535,000

Learn More

Youngtown TAS – 2 bed 1 bath house

Youngtown TAS 7249

Tax Depreciation Report

T.D$169,867 over 40 years

Purchase Price: ~$275,000

Learn More

McDonald Restaurant Minyama QLD

Minyama QLD 4575

Tax Depreciation Schedule

T.D$3,410,588 over 40 years

$4,900,000 total for the three site

Learn More

Japanese Restaurant Caloundra QLD

Caloundra QLD 4551

Tax Depreciation Schedule

T.D$246,823 over 40 years

Learn More

Warehouse Rowville VIC

Rowville VIC

Tax Depreciation Report

T.D$375,347 over 40 years

$780,000

Learn More

Emerald Airport Asset Revaluation

Emerald QLD 4720

Asset Revaluation, Tax depreciation

T.D$29.452.575 total depreciation

Learn More

Multi Tenanted Shops Burleigh Waters QLD

Burleigh Heads QLD

Tax Depreciation Report

T.D$363,912 over 40 years

$1,200,000

Learn More

Roll’d Elanora QLD

Elanora QLD

Tax Depreciation Schedule

T.D$172,607 over the 1st financial year

$379,000

Learn More

Factory Warehouse Caboolture QLD

Caboolture QLD

Tax Depreciation Schedule

T.D$45,214 over 40 years

$269,000

Learn More

Ground floor Retail and Cafe Shops Sydney NSW

Sydney NSW 2000

Tax Depreciation report

T.D$805,573 over 40 years

$3,570,000

Learn More

Bake Boss Clarence Gardens SA

Clarence Gardens SA 5039

Tax Depreciation Schedule

T.D$371,700 over 40 years

$1,800,000

Learn More

EzyMart Store Sydney NSW

Sydney NSW 2000

Tax Depreciation Schedule

T.D$279,170 over 40 years

$1,750,000

Learn More

Comfort Inn Coober Pedy Experience

Coober Pedy SA 5723

Task Depreciation Schedule

T.D$375,770

$600,000

Learn More

Office space Sunnybank QLD

Sunnybank QLD 4109

Tax Depreciation Schedule

T.D$147,548 over 40 years

$146,173

Learn More

Supermarket Deception Bay QLD

Deception Bay, Qld 4508

Tax Depreciation Schedule

T.D$1,768,668 over 40 years

$3,500,000

Learn More

Lidcombe NSW – 3 Bed 2 Bath House

Lidcombe NSW 2141

Tax Depreciation Report

T.D$235,5719 for 30 years

$1,150,000

Learn More

Avalon By Mosaic – Arbor 3 bed unit

Maroochydore, QLD 4558

Tax Depreciation Report

T.D$592,206 over 40 years

$1,235,000

Learn More

Avalon By Mosaic – Arbor 2 bed unit

Maroochydore, QLD 4558

Tax Depreciation Report

T.D$391,507 over 40 years

$749,000

Learn More

Fan Arcade NT

Alice Spring, NT 0870

Tax Depreciation Schedule

T.D$781,183 over 40 years

1.088.768

Double Storey House NSW

Lidcombe, NSW 2141.

Tax Depreciation Report

T.D$235,719 over 40 years

$1,150,000

Mercato on Ferry

Southport QLD 4215

Tax Depreciation Management

T.D$7,447,218 over 40 years

$18,272,008

Learn More

Glenrose Village Shopping Centre

Belrose NSW 2085

Tax Depreciation Management, Tenant Abandonment

T.D$55,321,172 over 40 years

$74,360,811

Learn More

Brisbane Fortitude Valley Metro

Fortitude Valley QLD 4006

Tax Depreciation, Tenant Abandonment

T.D$18,560,005 for over 40 years

$96,000,000

Learn More

Office Fitout – Mackay

Mackay QLD 4740

Tax Depreciation Report

T.D$2,324,626 over 40 years

$3,110,869

Learn More

Flinders Arcade – SA

Victor Harbor SA 5211

Tax Depreciation Report

T.D$64,289 over 29 years.

$165,000

Learn More

Marryatville Hotel

Kensington SA 5068

Depreciation Management

T.D$2,643,428 over 40 years

$3,525,000

Learn More

Flagstaff Hotel

Darlington SA 5047

Tax Depreciation, Asset Register, Depreciation Management

T.D$3,805,594 over 40 years

$7,550,000

Learn More

Mansfield Park Hotel

Mansfield Park SA 5012

Tax Depreciation, Asset Register

T.D$4,979,570 over 40 years

$5,005,080

Learn More

The Seaton Hotel

Seaton SA 5023

Tax Depreciation, Depreciation management

T.D $3,262,738 over 40 years

$6,100,000

Learn More

The Lion Hotel

North Adelaide

Tax Depreciation, Asset Register, Depreciation management

T.D$907,426 over 40 years

$5,500,000

Learn More

Tropical Gateway Motor Inn

Rockhampton

Depreciation management

T.D$701,422 over 40 years

$1,150,000

Learn More

Osborne Park – Warehouse & Office

Osborne Park WA 6017

Tax Depreciation Report

T.D$197,921 over 27 years

$1,220,000

Learn More

Byron Bay Pharmacy

Byron Bay NSW 2481

Tax Depreciation Report

T.D$533,667 over 40 years

$2,325,000

Learn More

Residential House – MacGregor ACT 2615

MacGregor ACT 2615

Tax Depreciation Report

T.D $44,990 over 40 years

$653,000

2012 Residential House

Rosebery, NT

Tax Depreciation Report

T.D$347,941 over 40 years

1990 Residential House

Oakhurst, NSW

Tax Depreciation

Curio by Mosaic – Apartment

Upper Mount Gravatt, QLD

Tax Depreciation

T.D$360,135 over 40 years

$490,500

Learn More

Norton Plaza Shopping Centre

Leichhardt, NSW

Tax Depreciation, CAPEX, Fit-out

T.D$44,372,381 over 40 years

$153,200,000

Learn More

Eliza Square Shopping Centre

Mount Eliza, VIC

Tax Depreciation, CAPEX Work

T.D$18,642,093 over 40 years

Learn More

St Helena Mediplex – Medical Centre

St Helena, VIC

Tax Depreciation, Capital Works

T.D$1,614,944

$6,700,000

Learn More

Novotel Southbank

South Bank, Brisbane

Tax Depreciation, CODE Management

T.D$59,152,226 over 40 years

$59,162,191

Learn More

Budds Backpackers

Gold Coast, QLD

Amendments of previous tax returns, Write off expenditure

T.D$1,270,353 over 40 years

Learn More

Cornerstone Village Pimpama

Pimpama, QLD

Tax Depreciation Reports

Large Industrial Unit – Kingsgrove NSW

Kingsgrove, NSW

Tax Depreciation, Acquisition Report

T.D$3,901,786 over 40 years

$37,000,000

Learn More

Office Fitout – Bank of Queensland HQ

Newstead QLD

Tax Depreciation

Office Fitout – Aristocrat

Sydney, NSW

Tax Depreciation Schedule

House & Land Package

Point Cook, VIC

Tax Depreciation Report

Unit – Darwin CBD, NT

Darwin, NT

Tax Depreciation Report

568 Collins Street – High Rise Un

Melbourne, VIC

Tax Depreciation Report

1970s House – Sunnybank, QLD

Sunnybank, QLD

Tax Depreciation

Townhouse – Ellen Grove, QLD

Ellen Grove, QLD

Tax Depreciation

Architectural Home – Sydney, NSW

Cottage Point, Sydney NSW

Tax Depreciation Report

Zen apartments, Sydney NSW

Wentworth Point, NSW

Tax Depreciation Report

Dakabin Crossing Development

Dakabin QLD

Tax Depreciation Report

Brisbane Skytower

Brisbane CBD, QLD

Tax Depreciation Report

Hotel – Byron at Byron

Byron Bay, NSW

Tax Depreciation, CAPEX, Asset Register

T.D$29,217,967 over 40 years

$56,522,461

Learn More

Cafes / Food – Zaraffa’s Coffee Shop

Coffs Harbour, NSW

Tax Depreciation, Capital works

T.D$839,096 over 40 years

Learn More

Education – Dr Du Centres

Sydney, NSW

Tax Depreciation, CAPEX, Write-off

Boutique Hotel – Little Albion Street

Sydney, NSW

Tax Depreciation, CAPEX, Asset Register

T.D$27,750,000

$10,162,104

Learn More

Foster & Partners Architects

Sydney, NSW

Tax Depreciation

T.D$279,170 over 40 years

$1,750,000

Learn More

Flynn Hotel

Cairns , QLD

Tax Depreciation, Asset Registers

T.D$152,769,314 over 40 years

$159,137,014

Learn More

The Bailey – 5 Star Hotel

Cairns , QLD

Tax Depreciation, Asset Register

T.D$97,062,605 over 40 years

$97,550,746

Learn More